For years, investors have searched for ways to gain exposure to SpaceX. The company remained private while transforming the economics of space launches, building one of the world’s largest satellite internet networks and becoming one of Elon Musk’s most closely watched businesses. That long wait now appears to be ending, and the response from investors suggests demand has been building for far longer than many expected.

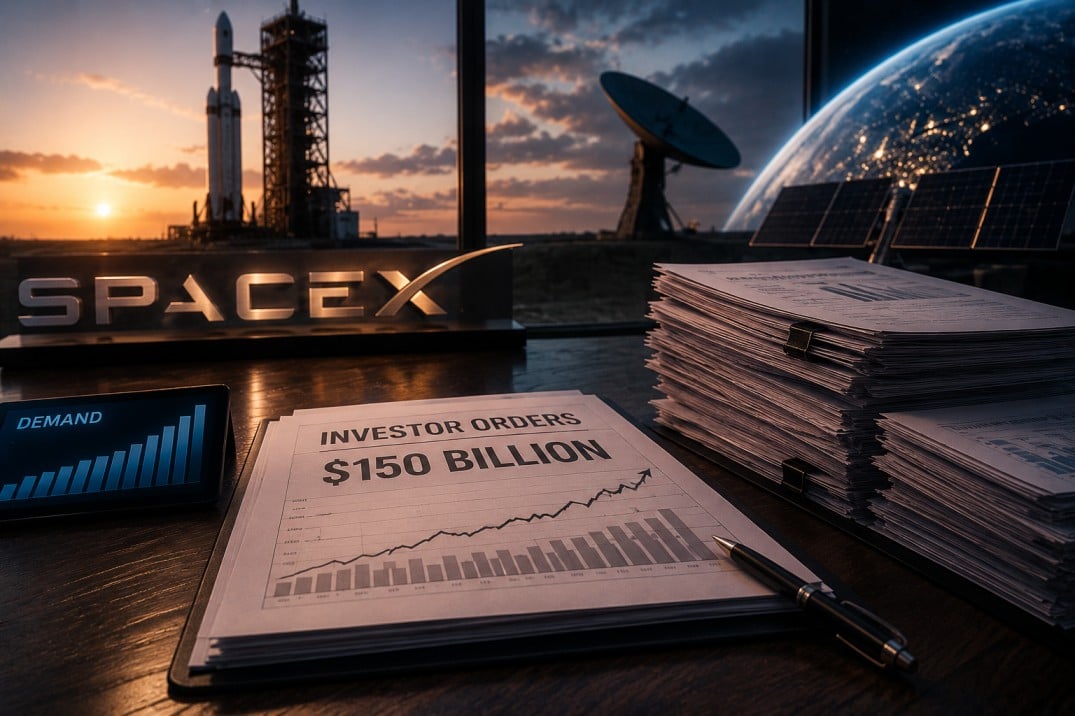

According to reports surrounding the company’s planned stock market debut, investor orders have reached roughly $150 billion ahead of the offering. The figure places SpaceX among the most sought-after public listings in recent memory and highlights the unusual position the company occupies in financial markets. Unlike many large businesses preparing to go public, SpaceX arrives with years of public attention, a recognised founder and a reputation built largely outside public markets.

Yet the sheer volume of investor interest tells only part of the story. The more important issue may be how little of the company is actually being offered to the market. Reports indicate that less than five per cent of SpaceX’s outstanding shares could be available in the flotation. That combination of enormous demand and limited availability has become one of the most closely watched features of the listing.

Investors are not simply examining launch revenues, satellite subscriptions or future earnings projections. Many are also responding to the fact that ownership of SpaceX has historically been restricted to private investors, venture capital firms and insiders. The public offering changes that equation, but only partially, because the supply of shares remains tightly controlled.

That dynamic has turned the upcoming listing into a test of how investors value access itself. In many public offerings, attention centres on growth rates, profit margins and market opportunities. In the case of SpaceX, part of the attraction appears to be the rarity of the asset being offered.

Limited share supply fuels intense investor competition

Public offerings often attract attention when they involve large companies or well-known brands. What makes the SpaceX listing unusual is the apparent imbalance between demand and the number of shares available.

If reports of a $150 billion order book are accurate, many investors seeking shares may receive only a fraction of what they requested. Such situations can create unusual trading conditions because buyers continue competing for ownership while the number of available shares remains relatively small.

Market history offers examples of highly anticipated listings where limited public floats contributed to sharp price movements after trading began. In those situations, investor enthusiasm can become concentrated in a small pool of stock, producing price swings that are not always linked directly to company fundamentals.

The SpaceX offering arrives with several ingredients that often attract investor attention. The company has become a dominant force in commercial space launches. Starlink has developed into a major satellite communications business. The company is also associated with projects ranging from lunar missions to long-term plans involving deep space exploration.

For many investors, however, the attraction may be simpler. SpaceX has been one of the most difficult major technology companies to access through public markets. Ownership was largely reserved for private market participants, leaving retail investors on the sidelines while the company’s valuation climbed steadily over the years.

That history has created years of pent-up demand. Investors who followed the company’s development from Falcon rockets to Starlink deployments now see an opportunity to participate directly rather than through indirect holdings or private market vehicles.

The involvement of Elon Musk adds another layer to the story. Musk has demonstrated a repeated ability to attract investor attention across multiple businesses, from electric vehicles and artificial intelligence to social media and space technology. His presence alone tends to draw interest from both institutional and retail investors.

Supporters argue that Musk’s businesses benefit from close relationships between companies that share technology, personnel and resources. Critics question whether those links make valuation more difficult and raise governance concerns that deserve closer examination.

The SpaceX prospectus reportedly highlighted commercial relationships with other Musk-linked businesses, including purchases involving Tesla products. Such transactions are legal when disclosed appropriately, but they often attract attention because investors seek clarity regarding financial relationships between related companies.

Questions over valuation and governance remain part of the discussion

The reported valuation target of approximately $1.8 trillion has also become a major talking point. That figure places SpaceX among the most highly valued companies in the world and far above some independent estimates produced by analysts and investment firms.

Differences in valuation assessments are not unusual, particularly for businesses operating in emerging industries. The challenge lies in determining how much value should be assigned to future opportunities that remain years away from generating measurable financial returns.

SpaceX presents investors with several businesses under one corporate roof. There is the launch business, which has already transformed the commercial space industry. There is Starlink, which continues to attract subscribers across multiple countries. There are also projects involving satellite services, data transmission and longer-term space-related commercial activities.

Investors must decide how those activities fit together and what assumptions should be made regarding future revenue generation. Some view the company as a transportation and communications business. Others see it as a broader technology company with ambitions extending into several industries.

Governance questions have also entered the discussion. Reports suggest Musk will retain overwhelming voting control after the listing, allowing him to maintain authority over major corporate decisions. Such arrangements are common among founder-led companies, though they often prompt debate about shareholder influence and accountability.

None of these issues appear to have reduced demand so far. Instead, investor interest seems to have strengthened as the offering approaches. The combination of a well-known founder, a business associated with major technological achievements and limited public availability has created conditions rarely seen at this scale.

{kind=link}