Excerpting from the JPM note, Feroli composed that the purchaser cost file (CPI) probably expanded 0.8% in May, over the 0.7% exp. furthermore, up from 0.3% in April. This hop will be because of a solid expansion in energy costs (4.6%) — as fuel costs expanded perceptibly again that month — alongside proceeded strong increases in food costs (0.7%) and the center record (0.47%). With this figure, JPM anticipates that the year prior CPI expansion should hold at 8.3% between April and May, at the end of the day, unaltered from last month and furthermore over the Wall Street agreement gauge of 8.2%.

Balancing JPM’s title agony, the bank expects some control in the center list, which it sees facilitating from 6.2% Y/Y in April to 5.8% Y/Y, beneath the 5.9% Wall Street agreement.

Boring down on the center print, JPM said it searches for “strong cost increments” across a significant number of the vitally basic classifications. While lease measures have been firm recently, the bank anticipates that strength should go on into May, with occupants’ lease-up 0.49% and proprietors’ identical leases expanding 0.45%.

It deteriorates: Feroli takes note that housing costs likewise have hopped of late as movement action bounced back from the COVID-related shock and he searches for one serious area of strength for more in May, with costs up to another 2.0%. Simultaneously, public transportation costs likewise have risen fundamentally of late, which probably reflects expanded interest for movement and higher fuel costs; JPM expects a 1.5% increment in open transportation costs to be accounted for in May.

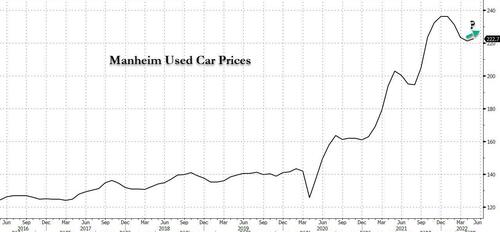

It deteriorates, with JPM next zeroing in on vehicle costs which have been in concentrate of late, with a flood in costs detailed as of recently. And keeping in mind that signs looked blended in regards to the May information, the bank doesn’t anticipate that especially enormous changes should be accounted for the month, with new vehicle costs up 0.4% and, surprisingly, utilized vehicle costs moving unobtrusively higher once more.

At last, while by and large expansion has areas of strength for been, correspondence costs have dropped down as of late, and JPM anticipates that this descending pattern should go on into May, with a 0.2% decrease in costs during the month. Clothing costs likewise cooled in April following run areas of strength and we anticipate that an extra 0.1% downfall should be accounted for in May.

And keeping in mind that one can overlook JPM’s examination, doing so became hazardous when not long after the finish up with White Home authority emphasized the admonition that costs will come in hot, telling Fox News columnist Edward Lawrence that the White House anticipates “title expansion will be raised on the grounds that gas costs were 8.5% were more prominent in April than May. The White House Official says that will saturate CORE expansion through aircraft tickets due to the cost of fly fuel.”

Obviously, the administration couldn’t leave it on such a troubling note and let Lawrence know that the White House is following a shift in ways of managing money from purchasing merchandise to purchasing administrations, which they accept will ease the strain on supply chains as cash moves from purchasing stuff to purchasing administrations.

At last, when inquired as to whether the US is in a downturn, the White House Official said that additions in the work market and interest for merchandise don’t show we are in a downturn. They said it is “improbable”. Official says the organization is in a “great spot to change” the economy to stable development. This is extraordinary information, since deciding how horrendous the White House has been in its financial evaluation of, indeed, anything, the US should now currently be in a profound downturn (on the off chance that not sorrow) and the ongoing explosion of expansion is going to get Lehman as it did in 2008.

What’s more, with both Lehman and the White House saying CPI will beat assumptions, we are taking the under.

{kind=link}