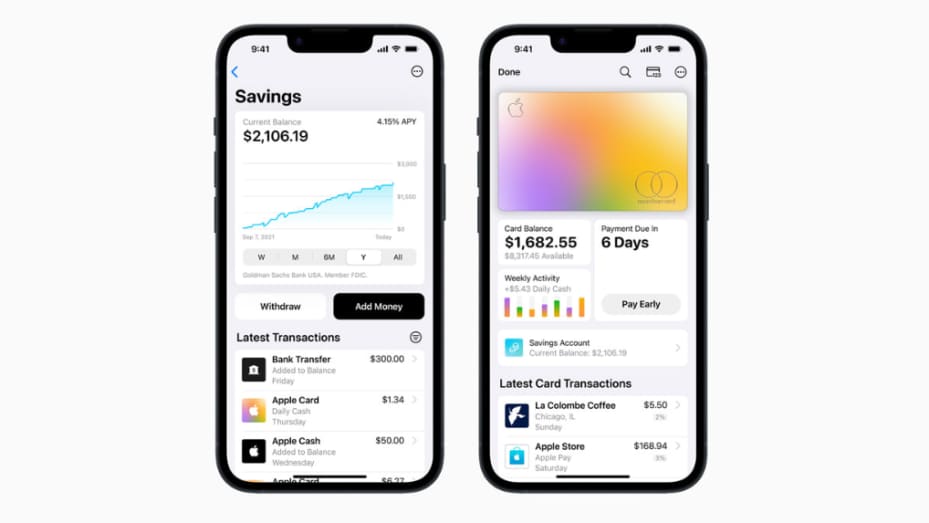

Apple has launched its Apple Card savings account with an annual percentage yield (APY) of 4.15%, significantly higher than the national average of 0.35%, according to the Federal Deposit Insurance Corporation. The savings account can be set up from the iPhone Wallet app and requires no minimum deposit or balance. Users can add funds from their bank account to build on their earnings, and all Daily Cash rewards earned through the Apple Card will be automatically deposited into the savings account. Daily Cash is the Apple Card reward program that offers up to 3% back on purchases.

The Apple Card savings account is launched in partnership with Goldman Sachs, which also provides the Apple Card credit card. The move represents a further expansion into the financial services industry by the tech giant, which already offers Apple Pay and the Apple Card credit card. However, competing savings accounts provided by large credit unions, online banks, and brick-and-mortar banks can offer customers significant APYs.

The cashback earned through Apple Card savings is called “Daily Cash” and is automatically added to users’ Apple Cash balance, which can be used for other purchases, sent to friends or family, or transferred to their bank account. Apple Card savings is a simple and convenient way for Apple Card users to earn cashback on their everyday purchases and accumulate savings.

For example, CIT Bank offers a savings account with a 4.75% APY when customers deposit a minimum of $5,000. Marcus by Goldman Sachs has a 3.9% APY with no minimum balance or monthly fees. Capital One’s savings account has no minimum balance, and users can earn a 3.5% APY. Vio Bank offers a savings account with a 4.77% APY with no minimum balance.

Continuing the Success, Apple Card Savings Account Joins the Apple Card Family

Users of the Apple Card savings account can manage their accounts through a dashboard in the Wallet app, where they can track their interest and account balance or withdraw funds. The move comes as traditional banks face growing competition from tech companies like Apple, which are leveraging their large user bases and innovative technology to offer financial services.

Apple’s move into financial services has been driven by a desire to diversify its revenue streams beyond hardware, such as iPhones and Macs, and to tap into the lucrative financial services industry. The company has positioned itself as a trusted brand, with a focus on user privacy and security, which could give it an advantage in the highly competitive financial services industry.

The Apple Card savings account launch follows the successful rollout of the Apple Card credit card in 2019, also issued in partnership with Goldman Sachs. The Apple Card offers users up to 3% back on purchases, with no annual or penalty fees. The credit card also comes with a number of unique features, such as the ability to track spending and view transaction histories in real time.

The tech firm focuses on user privacy and security, making it an advantage for the users

However, the Apple Card credit card launch has been subject to controversy. In 2019, it was reported that the credit limit offered to women was lower than that provided for men, leading to accusations of gender bias. In response, Apple promised to re-evaluate its credit scoring algorithm to ensure gender equality.

Overall, the launch of the Apple Card savings account represents Apple’s further expansion into the financial services industry, leveraging its large user base and innovative technology to offer customers a competitive APY. While other savings accounts offer higher APYs, Apple’s trusted brand and focus on user privacy and security could give it an advantage in the highly competitive financial services industry.

{kind=link}