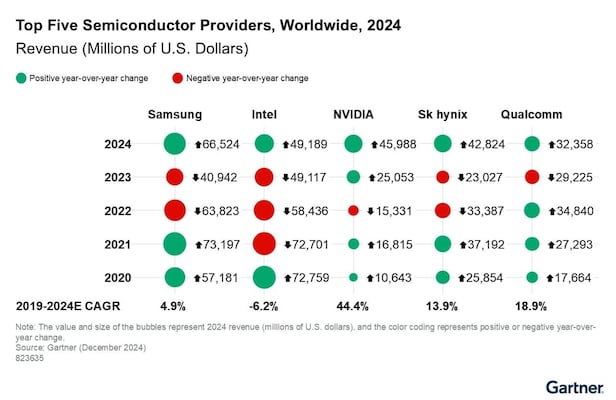

Following a recent market analysis done by Gartner, Samsung Electronics is projected to regain its position as the top semiconductor vendor in the world in 2024, just ahead of Intel.

This could indicate a change for the better after Samsung has been struggling with slipping profit margins within its DRAM and NAND flash divisions. Company sales of semiconductors are projected to hit around $66.5 billion, an astonishing 62.5% increase year over year.

Intel Faces Challenges as Samsung Takes the Lead

Gartner pointed out that for Samsung, this resurgence is fueled largely by a strong recovery of previously declining sales of memory chips. From what the firm expects, Samsung has also foreseen to have a five-year CAGR of 4.9% by the end of 2024.

This shift is unprecedented not just for Samsung, but for the semiconductor sector as a whole which witnessed global turnover growing from $530 billion in 2023 to $626 billion in 2024, which is an 18.1% growth.

Intel, which had been the top vendor in semiconductor sales in 2023, is forecasted to fall to second place with sales of $49.2 billion, reflecting a marginal increase of 0.15%.

The company has been experiencing tremendous challenges, including large-scale layoffs and a strategic shift under new leadership following the exit of CEO Pat Gelsinger after four years in office.

AI Drives Semiconductor Reshuffle

Nvidia is also making waves in the semiconductor industry and is expected to move into third place with estimated sales of $46 billion. This is mainly because of the explosive demand for semiconductors for AI, namely graphics processing units (GPUs) and data center AI processors.

In the meantime, SK Hynix is expected to rise two spots to fourth position, thanks to its dominance in the high-bandwidth memory (HBM) market, which has been growing at a breakneck speed as demand for artificial intelligence technologies grows.

The HBM space has become steadily more important with the growing traction of generative AI systems in every industry. Revenue for SK Hynix stands at $42.8 billion, a massive year-over-year improvement of 86%. Gartner credits this upswing to mounting average selling prices (ASP) on memory products coupled with SK Hynix’s leadership in HBM applications specialized for AI.

TSMC Dominates, Despite Rankings

Note that Taiwan’s TSMC, the largest foundry in the world to specialize in semiconductor contract manufacturing, was not included in Gartner’s rankings. Nonetheless, TSMC posted a huge annual net sales growth of 33.9% to around $88.6 billion. TSMC would be the top dog in global semiconductor sales if included in the rankings.

The semiconductor sector continues to deal with a convoluted environment marked by changing demand and advancing technological requirements. While Samsung Electronics is poised to make its return as the dominant supplier, Intel continues to battle challenges that can stall its comeback plans.

The emergence of the likes of Nvidia and SK Hynix points to the evolving dynamics in the market, especially with AI technologies leading to increasing demand for bespoke chips.

As we progress deeper into 2025, industry players will be keenly observing these developments and their ramifications for future growth patterns in the global semiconductor industry.

{kind=link}