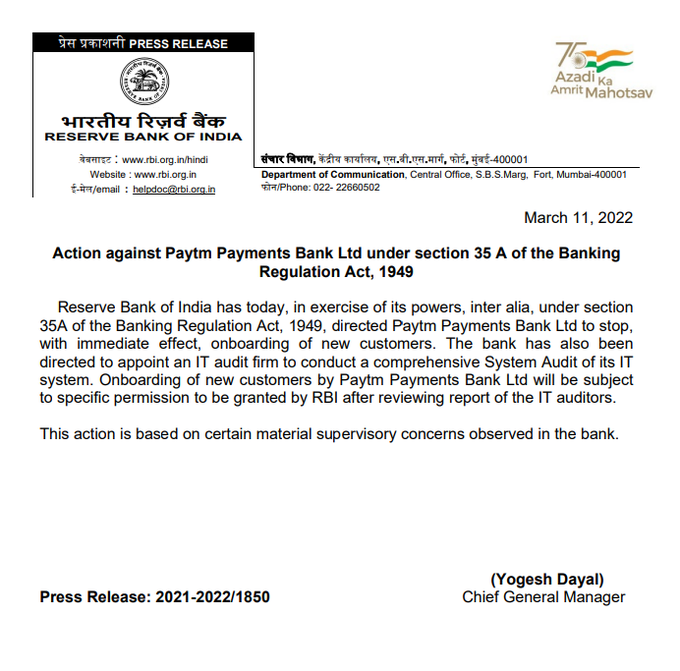

“The Reserve Bank of India has today (March 11), in the exercise of its powers under section 35A of the Banking Regulation Act, 1949, advised Paytm Payments Bank Ltd to cease onboarding of new clients with immediate effect,” the RBI said in a circular.

HIGHLIGHTS

- The Reserve Bank of India (RBI) barred Paytm Payments Bank from accepting new customers on Friday.

- The RBI has also ordered that the bank employ an audit company to conduct a system audit of its IT system.

- This action is being taken in response to material supervisory concerns raised by the bank.

It further stated that Paytm Payments Bank’s onboarding of new customers will be subject to particular clearance from the RBI after reading the IT auditors’ report. This move is based on “some serious supervisory issues discovered in the bank,” according to the statement.

While the RBI did not explain why it is preventing the firm from accepting new customers, this is not the first time the regulator has taken such an action. In August 2018, it was reported that PayTm Payments Bank has ceased enrolling new clients as a result of an RBI audit, which indicated that the company was not adhering to adequate know-your-customer (KYC) rules when it came to obtaining new consumers.

RBI Bars Paytm Bank from Taking New Customers

Later, it was discovered that the RBI was also concerned about the close relationship between Paytm Payments Bank and its parent company, One97 Communications because Payments banks are obliged by law to maintain an arm’s length distance from promoter group firms. Paytm parent company One97 Communications owns 49 percent of Paytm Payments Bank, while Paytm founder Vijay Shekhar Sharma owns 51 percent.

According to reports, the firm failed to meet the Rs 100-crore net worth criteria and was also exceeding the Rs 1-lakh deposit limit allowed per account for payments banks at the time. PayTm did not respond when contacted at the time this story was initially published.

{kind=link}