The economic crisis in the United States is having a significant impact on it’s households as the latest reports suggest that nearly two-thirds of households in the country are now living paycheck to paycheck. Increasing prices of goods and services due to high inflation in the economy are stated as major reasons for the increase in the number of people who have to live paycheck to paycheck.

What is paycheck to paycheck?

‘Paycheck to paycheck’ is a situation when an individual or a household completely relies on their monthly paycheck (wages, salaries, compensation, etc) to meet up the expenses of the household. In this situation, the individual or household will not be able to make any significant savings for the future.

2022 report

According to the results of a 2022 study conducted by LendingClub, nearly 64% of Americans had to live paycheck to paycheck last year. LendingClub is a financial services company based in San Francisco, California. If the numbers put out in the survey are accurate, it means that nearly 166 million people in America are currently using up all their salaries and wages on living expenses without any scope for savings.

In 2021, almost 61 percent of households in the United States were in this situation while in 2020 it was near the levels of 2022. In 2020, covid 19 pandemic and the resultant lockdown had deep impacts on the economical position of households.

Even $100000 is not enough

In the survey that included 3,989 US consumers, more than half of people who earn above 100000 dollars said that they were also facing issues with handling expenses and that they are also living paycheck to paycheck. 51 percent of consumers who earn above 100000 dollars said they also lived paycheck to paycheck.

The 51 percent rate in this category of six-digit earners signifies a big jump from 42 percent in 2021.

What led to this situation?

Russian special military operation in Ukraine and sanctions on oil and gas from Russia had resulted in high prices for oil in the international market. Worries of supply shortage resulted in fuel prices skyrocketing in the world market.

This sudden hike in prices resulted in a 40-year high inflation rate in the United States. Along with fuel, other essential commodities and services such as food, electricity, furniture, and many more witnessed a steep increase in prices.

As inflation skyrocketed in the economy, individuals and households were forced to spend more on essential commodities and cut spending on other items such as automobiles, trips, luxurious commodities, etc.

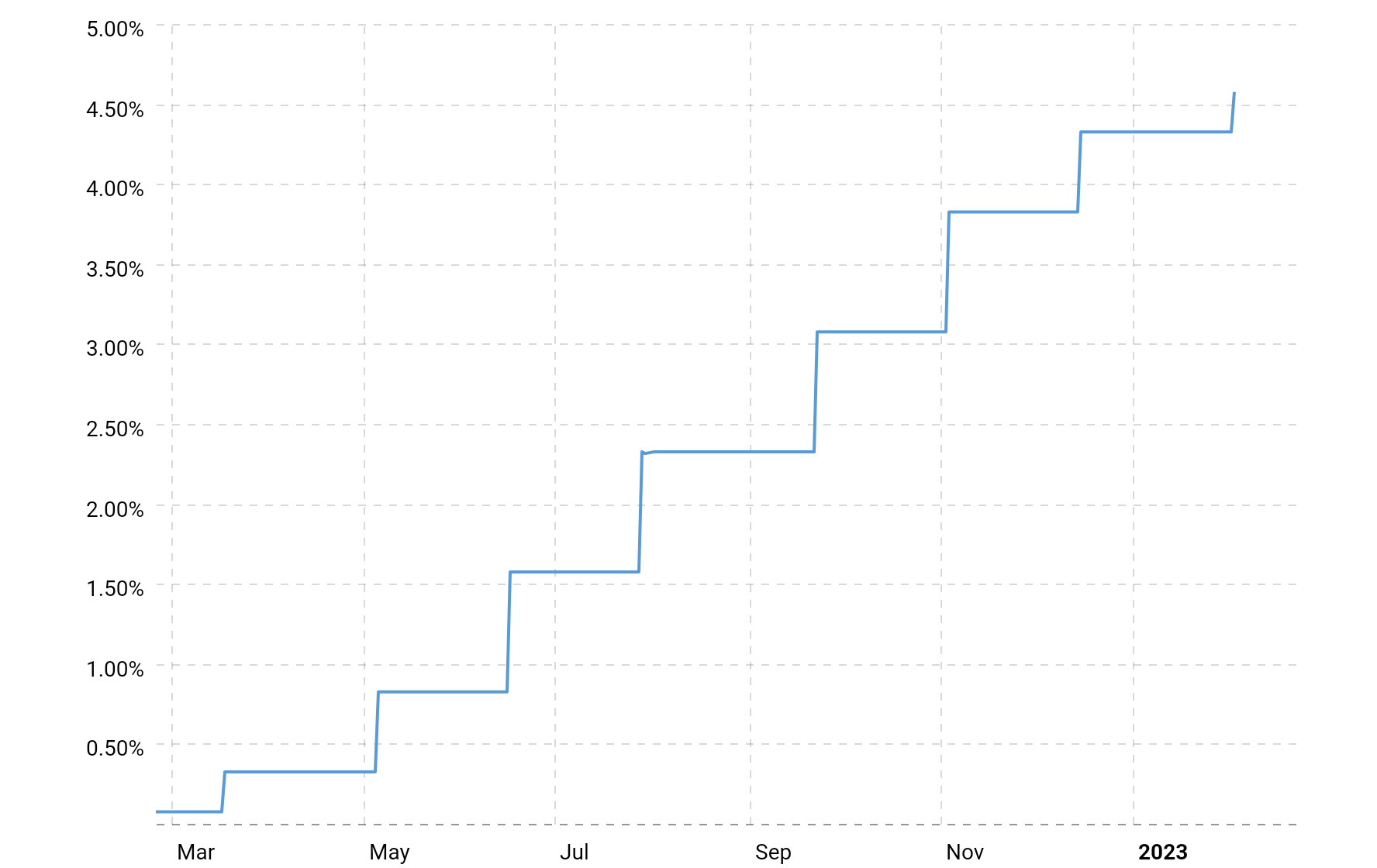

US Federal Reserve and High cost of debt

To bring down inflation in the economy, the Central Bank of the country and the Federal Reserve decided to increase interest rates in the economy. Back-to-back interest rate hikes pushed up lending rates. The cost of debt in the country increased at historical levels.

Credit Card debt getting bigger and bigger

According to a report by TransUnion total credit card debt in the United has touched $930.6 billion at the end of 2022, an 18.5% spike from a year earlier. The average balance has also increased to nearly $5,805 over the past 12 months.

This unexpected increase in credit card debt was triggered by the increasing cost of living in the country. Reports suggest that credit card holders are using the cards to meet day-to-day shopping expenses.

According to a report by Bankrate, the share of credit card users who carry forward payment balances to the next month has increased to 46% from 39% a year ago. This will make the financial situation of the individual/household worse as interest rates on credit cards are skyrocketing in the country.

Even individuals who make $100,000 or more in a year are finding it difficult to pay their credit card bills completely. Usually, it is people in the low-income category who breaks payment of monthly credit card bill.

Banks are preparing for the worst-case scenario

As credit card debt is on an unprecedented rise, banks across the United States are preparing for the worst-case scenario. During the release of fourth-quarter, earnings report,s heads of major banks in the United States, JPMorgan Chase & Co., Bank of America Corp., Wells Fargo & Co., and Citigroup Inc said that credit card debt of customers is increasing and that many finding it difficult to make the bill payments.

In the fourth quarter, these four banks set aside $6.18 billion in provisions for bad loans.

Reports suggest that banks will continue setting aside a large amount of money as a provision for bad debt, to cope with any credit card debt repayment crisis in the upcoming months.

{kind=link}