The Cava business model is one of the most studied success stories in modern fast-casual dining and for good reason. In less than two decades, Cava Group transformed from a neighborhood Greek restaurant into a category-defining Mediterranean powerhouse, generating over $1 billion in trailing annual revenue and commanding a market valuation that rivals brands with decades more history. If you have ever wondered what makes the Cava business model tick, you are looking at one of the most compelling case studies in how food, technology, and brand identity can combine to create durable enterprise value.

This deep-dive unpacks every dimension of how Cava makes money: its core restaurant operations, its consumer packaged goods (CPG) channel, its digital ecosystem, its unit economics, and the long-term expansion blueprint that has Wall Street buzzing about whether it can replicate or even surpass Chipotle’s legendary growth trajectory.

The Founding Story: From Mezze to Mainstream

Cava’s story begins on September 5, 2006, when three first-generation Greek-American friends Chef Dimitri Moshovitis, Ike Grigoropoulos, and Ted Xenohristos opened the first Cava Mezze in Rockville, Maryland. The concept was rooted in elevating Mediterranean flavors: fresh olive oil, legumes, grilled proteins, and signature chef-made dips like Crazy Feta, spicy hummus, and tzatziki.

The early years were anything but glamorous. The founders moved in with their parents, had no sign, no POS system, and ran the restaurant by hand. But the food found its audience, and the revenue grew. When co-founder Ike Grigoropoulos an accountant by training began managing finances more seriously, the business started generating real profit, which funded the opening of a second location.

By 2011, recognizing demand for their popular dips and spreads, the team made a pivotal strategic move: entering the consumer packaged goods market. Their dips began appearing on shelves at Whole Foods Market. Also in 2011, Cava pivoted from a full-service mezze model to a high-throughput fast-casual concept the architectural turning point that unlocked scale.

The most transformative external move came in 2018: Cava acquired Zoës Kitchen a Texas-based Mediterranean fast-casual chain for $300 million, gaining over 250 locations nationwide and instant national scale. On June 15, 2023, Cava Group debuted on the New York Stock Exchange, pricing its IPO at $22 per share, opening at $42, and closing at $43.78 a 99% first-day gain.

Cava Group expansion timeline from Rockville 2006 to Project 1000 by 2032

How the Cava Business Model Works

At its core, the Cava business model rests on three interlocking pillars: fast-casual restaurant operations, a consumer packaged goods segment, and a digital-first engagement strategy. Each reinforces the others in a flywheel dynamic that builds brand recognition, customer frequency, and margin efficiency simultaneously.

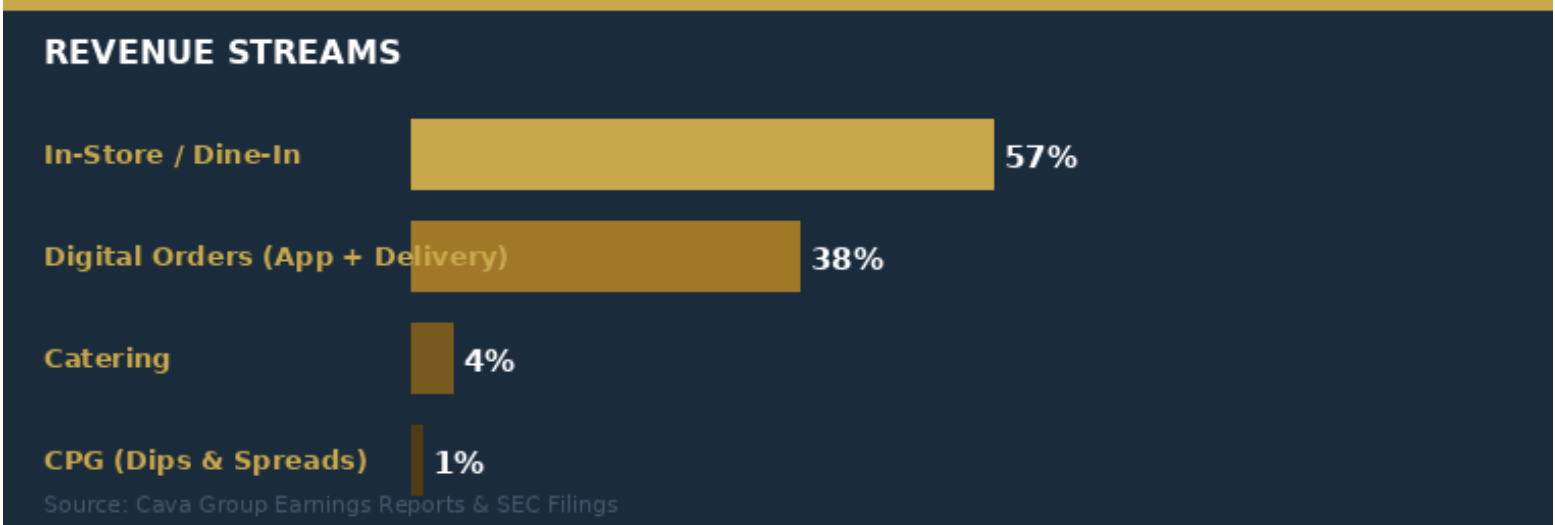

Cava revenue streams restaurants dominate at 95%+ with digital orders comprising 38% of the mix

Pillar 1: Fast-Casual Restaurant Operations

Restaurant sales account for over 95% of Cava’s total revenue. The format centers on an assembly-line, build-your-own-bowl model: customers walk down a serving line and customize their meals from Mediterranean bases (grains, greens, or pita), premium proteins (grilled chicken, falafel, steak), and over a dozen fresh toppings and signature dips.

The check architecture is deliberately tiered. A standard bowl runs $11–$13, but premium proteins and add-on dips (such as the $1.50 avocado option) lift the average check to roughly $13.50–$15.00 per customer. All Cava restaurants are company-owned ensuring full control over the customer experience, food quality, and brand consistency, with margin improvements flowing directly to the company as unit count grows.

Cava serves customers across all age groups, income brackets, and backgrounds, benefiting from growing demand for healthy food and a demographic shift toward greater appreciation of Mediterranean cuisine. The broad appeal accommodating vegetarians, vegans, carnivores, and gluten-free diners alike is a structural competitive advantage.

Pillar 2: Consumer Packaged Goods (CPG)

Cava’s CPG segment consisting of signature dips and spreads including Crazy Feta, harissa, hummus, and tzatziki operates in more than 650 premium grocery doors, including Whole Foods and Amazon Fresh. The company opened a 55,000 square-foot production facility in Virginia in 2024 to handle in-house manufacturing. While CPG is a small fraction of total revenue, it functions as a high-margin marketing vehicle: retail shoppers discover Cava in grocery aisles, become fans of a specific dip, and are organically converted into restaurant visitors a two-way flywheel.

Pillar 3: Digital Revenue and Technology

Digital revenue accounts for 38% of total sales comparable to Chipotle, which operates more than 3,200 locations. Cava built an in-house microservices platform powering its mobile app, digital ordering website, and point-of-sale system. Third-party delivery through Uber Eats, DoorDash, and Grubhub contributes approximately 30% of total sales. A revamped loyalty program with approximately 8 million members drives 25% higher annual spending versus non-members.

Unit Economics: The Numbers Behind Each Restaurant

Average Unit Volume (AUV): As of 2025, Cava’s restaurants generate approximately $2.9 million in average unit volume per year a standout figure reflecting strong customer traffic and efficient throughput.

Restaurant-Level Profit Margin: In Q1 2025, Cava posted a 25.1% restaurant-level profit margin virtually identical to Chipotle’s 26.2% in the same quarter. As one analyst noted, “at the store level, Cava’s unit economics are virtually identical to Chipotle’s” an extraordinary achievement at a fraction of Chipotle’s scale.

Revenue Growth: Total revenue for fiscal year 2024 reached $954.3 million, a 33.1% increase. In Q1 2025, revenue hit $328.5 million, representing 28.2% year-over-year growth. By trailing twelve-month calculations, Cava surpassed $1 billion in annualized revenue by mid-2025.

Balance Sheet: Cava carries no debt and holds approximately $386 million in cash, providing substantial flexibility to fund expansion without dilutive equity raises or leverage risk.

| Revenue Stream | Approx. Share | Key Driver |

| Restaurant In-Store Sales | ~57% of total | Walk-in dine and assembly line throughput |

| Digital / Online Orders | ~38% of total | App, website, and delivery platform orders |

| Catering | ~5% and growing | Corporate and event orders |

| CPG (Dips & Spreads) | < 1% of total | Retail grocery shelves, Whole Foods, Target |

Technology and the Connected Kitchen Initiative

Behind every bowl Cava serves is a surprisingly sophisticated technology stack. The Connected Kitchen initiative uses AI-driven predictive modeling to optimize prep lists, inventory management, and labor deployment during peak periods. AI models analyze historical order flow and real-time digital data to generate dynamic kitchen prep lists, reducing per-store food waste and smoothing throughput during the lunch and dinner rush.

A new labor-scheduling system rolling out across the network uses live digital order data to right-size staffing, improving labor efficiency and reducing overtime costs. The company is also piloting Cava Pick-Up windows and digital drive-through lanes in suburban locations, capturing convenience-oriented demand and increasing ticket throughput during peak hours.

Expansion Strategy: Project 1000 and Beyond

Cava’s most ambitious strategic declaration is what observers have dubbed Project 1000 the company’s stated goal of reaching 1,000 U.S. restaurant locations by 2032. As of mid-2025, with roughly 400 locations operating across 26 states and Washington D.C., this requires more than doubling the restaurant footprint in approximately seven years.

The expansion map is deliberately targeted. Cava’s historical strength has been in the Northeast, Mid-Atlantic, and Sun Belt. The company is now aggressively pursuing the Midwest and Pacific Northwest “white space” markets with minimal Mediterranean fast-casual competition and strong health-conscious consumer trends. For fiscal year 2025, Cava has guided at least 17% unit growth, equating to 62 to 66 new restaurant openings.

Restaurant format is also evolving. New openings increasingly feature Cava Pick-Up windows and digital drive-through lanes. Cava Catering a program requested since the company’s very first restaurant is now expanding as an incremental revenue layer. On the international front, Cava is exploring franchise and joint-venture pilots in Canada.

Competitive Positioning: The Chipotle Parallel

No analysis of the Cava business model is complete without the Chipotle comparison. The parallels are genuinely striking: both operate assembly-line customizable-bowl formats, both have invested heavily in digital ordering, and both have cultivated loyal, health-conscious customer bases. At the restaurant level, Cava’s 25.1% margin is virtually at parity with Chipotle’s 26.2%.

However, meaningful differences exist. Chipotle’s new-store break-even is 6 to 12 months versus 12 to 18 months for Cava, reflecting stronger national brand recognition. Chipotle’s AUV of $3,142 exceeds Cava’s $2,865. But Cava’s revenue growth of 28.2% in Q1 2025 dwarfed Chipotle’s 3.0% a 25 percentage point gap reflecting Cava’s earlier-stage, faster-expanding profile.

Key Risks and Challenges

- Valuation premium: Cava trades at a very high forward price-to-earnings multiple, leaving little room for execution missteps.

- Cost pressures: Food inflation (fresh produce, proteins, olive oil) and rising labor costs driven by minimum wage increases across key markets.

- New market execution risk: Entering the Midwest and Pacific Northwest where brand awareness is lower means longer new-store ramp times and higher marketing spend.

- Culture at scale: Cava leadership has explicitly cited preserving company culture as a key competitive advantage and a critical execution risk as the team grows rapidly.

- Competition: Sweetgreen and regional Mediterranean concepts compete for the same health-conscious fast-casual consumer.

Conclusion: Why the Cava Business Model Matters

The Cava business model is more than the sum of its revenue streams. It represents a well-constructed thesis about where consumer tastes, technology, and cultural trends are converging. A brand built around Mediterranean food historically a fragmented, regional category has become a scalable national enterprise with unit economics that match the best operators in the industry.

What makes the Cava business model particularly instructive is how it layers its monetization. Restaurants generate the volume. Digital channels improve margins by reducing dependency on third parties and building proprietary customer data. CPG products extend the brand beyond restaurant walls and lower customer acquisition cost. Catering adds a high-margin revenue layer. And loyalty ties it all together, converting single-visit customers into habitual Cava eaters who spend 25% more per year.

Whether Cava ultimately fulfills the Chipotle comparison or carves its own distinct legacy as the category-defining Mediterranean brand the mechanics of how it generates, retains, and grows revenue are a masterclass in modern fast-casual strategy.

{kind=link}