The Indian FinTech start-up environment is blossoming and bursting at its seams. Some of the more popular sub-sectors such as payments, e-commerce are close to saturation while other sub-sectors, including consumer and enterprise finance are yet to receive adequate start-up attention. Moreover, applications for newer technology such as Blockchain, AI, robo-advisory in investments are few and far between.

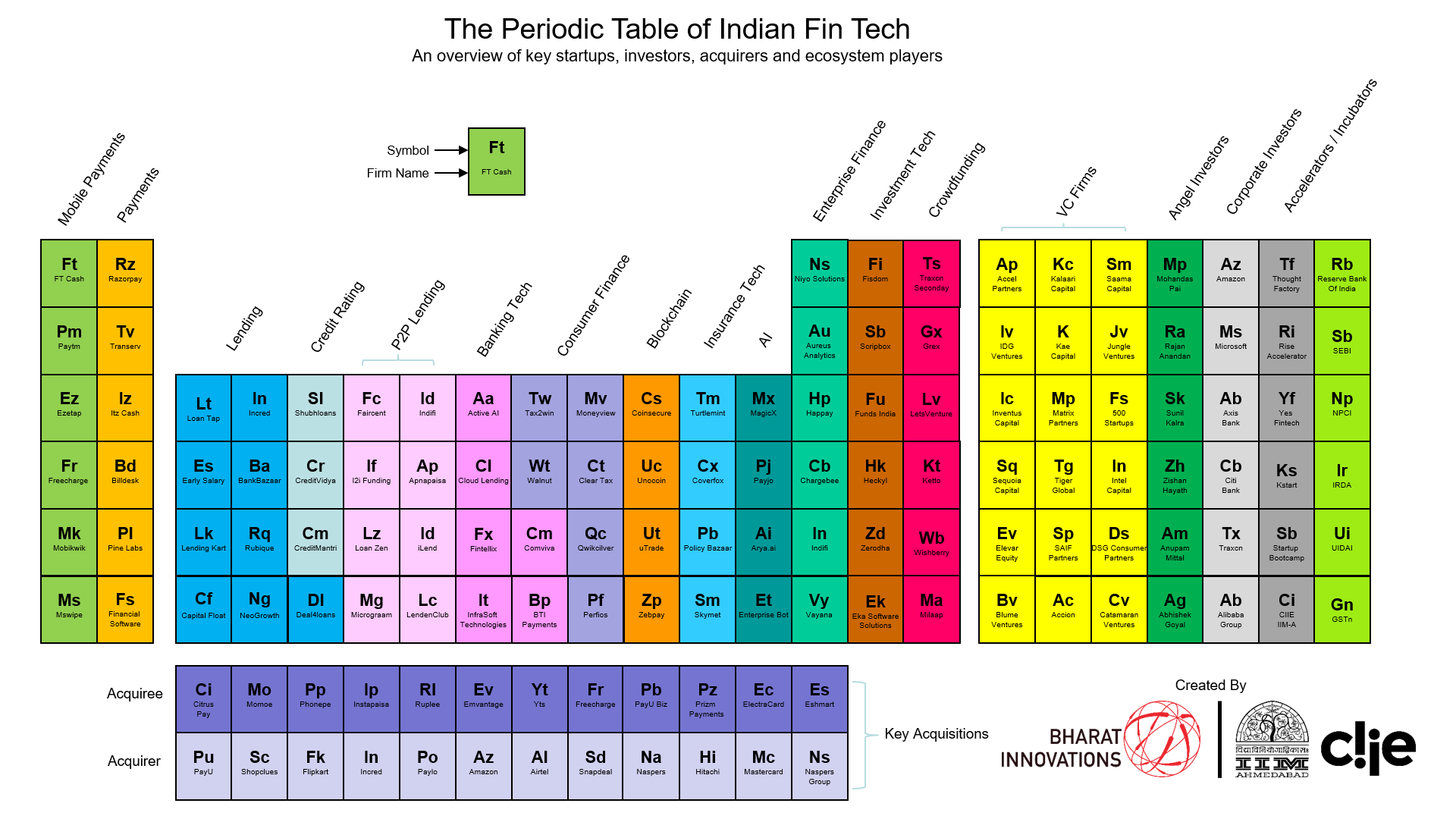

To understand the distribution better, we created a periodic table of FinTech start-ups in India covering start-ups and investors.

The 80 start-ups out of an initial list of 193 (as of 31st December 2016) have been chosen based on a combination of innovation, block score, (calculated using a range of metrics which include team size, funding, website visits, usage, social media followers, company mentions, app downloads, etc.) and funding status. The 30+ investors are chosen based on their investments activity.

By most measures, nearly two thirds of the Indian financial system is in the public domain. The government as its dominant shareholder is unable to provide adequate capital to enable banks to maintain market share in line with GDP growth.

The public sector, as a whole, has been losing market share in the financial sector at the rate of 1% per annum over the last decade. Given higher NPAs, higher growth and higher capital requirement that the government is unable to provide, it is expected that the market share of the public sector would continue to decline, perhaps by as much as 2% per annum.

This retreat of the dominant public-sector players, a rapidly growing market for financial services, the advances in technology and governmental interventions such as Aadhaar, India Stack, Jan Dhan, UPI present a unique opportunity for technology-led private sector players to make a mark in the financial services space.

Reading the periodic table

We split the FinTech space into 10 broad sub-sectors and 7 types of investors. Within each sub-sector/type the companies are sorted in ascending order by the block score. The more innovative and recently founded companies will show on the top, while older companies will be at the bottom.

This list is certainly not exhaustive and is expected to change over time with ever-increasing interest in India’s FinTech potential.

FinTech M&A Deals

The ongoing churn and consolidation different FinTech applications/services is represented as “transition elements” outside the main periodic table. The 12 acquisitions were selected based on the status and maturity of acquirers, and potential synergy of the deals. The number of deals and the involvement of bigger players in certain areas of M&A signify the level of saturation and scope for future growth.

For example, more than 50% of the deals considered were found in the Payments sub-domain (including Mobile Payments) compared to fewer deals in areas such as Insurance Tech, and Investment Tech underlining the underlying growth potential in the latter fields.

Key drivers in each sub-vertical

Every sub-sector is at a different level of saturation. Our study has identified the different drivers for each sub-sector depending on the maturity, internal constraints and external influences that govern that sub-vertical.

Mobile Payments: Cheap mobile phones, Increase in internet coverage, Support from regulatory authorities

The ubiquity of cheap mobile phones with some that cost a mere ₹1000 has made the long-tail of the Indian population accessible to a start-up that wants to enter the mobile payments space. According to the NITI Aayog report, number of non-cash payments transactions by non-banks per capita per annum is just 11 with just 1.08 pay points per million people (even China has 16k+). With telecom companies wanting to reach the remotest corners of the country, this number is expected to grow exponentially.

RBI is encouraging banks to adopt the Unified Payments Interface to provide the end-user with more flexibility in making inter-bank transfers. In October 2016, the total number of digital payments was ~ 900 million. This translates to about 1 transaction per adult per month for approximately 900 million adults. The government is currently targeting 30 billion digital payments a month by December 2017, i.e. one digital payment transaction per adult per day.

The infrastructure is getting better by the day with free urban Wi-Fi, rural broadband, Aadhaar based payment systems (AEPS). The people who are not reached by this effort are being brought in by USSD systems that don’t require Internet connectivity. Yet, India falls in the middle of the pack in terms of the Mobile Payments Readiness Index as measured by MasterCard pointing further to the unexploited opportunity

The confluence of accessible internet infrastructure, low-cost handsets and a push from the Government makes grain-sized payments a reality. This capability has formed a virtuous circle in mobile commerce. More sections of the population are getting accustomed to making purchases from their mobile phones. This in turn, forces businesses and financial institutions to respond to a growing need for simple and fast payment networks.

Payments: Increase in online shopping; Need to reach the interiors of India

Other than mobile payments, a whole range of payment methods drive start-ups to get creative with their offering. Payment providers and processors will have to adapt to the varied needs for customer payment methods – cash, wallets, credit and debit cards, wire transfers, etc. The trend towards seamlessness, inter-operability, and light-touch payment options is likely to continue across payment solutions.

Even if not new, banks have played a pivotal role in moving their customer base to digital payments. Digital offerings by traditional banks will create competition for start-ups, especially considering that they have a ready customer base.

If it wasn’t for the rise in online shopping, there wouldn’t be a digital payment space to discuss. An exponential increase in the number of social marketplaces and aggregators is the key to the rise in demand for digital payments.

Payment gateways have attracted suitable attention with start-ups we considered. While some might serve a niche such as financial institutions or only certain types of payments, most have a payment platform in some shape, size or form.

Tie-ups with payment wallets and credit card companies is wide-spread too. As this sub-sector matures we expect a lot more seamless applications leveraging Aadhaar or UPI to include the untapped high-volume, low-transaction-value population. Interestingly, social media applications like WhatsApp are believed to be developing un-intrusive, in-chat payment options using UPI.

Therefore, a start-up that offers a payment solution will have to differentiate itself from the many others who already co-exist in this space. On the other hand, financial inclusion of those who have not been touched by digitization is ripe for exploration. There are some creative applications in this space, such as money transfer without Internet (UltraCash) or cash on delivery models (GharPay).

Lending: Instalments for day-to-day payments; Need for credit scoring systems

The Government’s inclination to make micro-lending easier on the lender and more accessible to the borrower through its support to IndiaStack is apparent. Personal finance too has begun to enjoy regulatory leeway. Even with a healthy income stream, the burgeoning middle class in urban and semi-urban India faces short-term liquidity issues. This opens up a plethora of applications in avenues related to lending. An example is “Early Salary” that provides bridge financing till pay day.

In addition, unconventional loan opportunities have sprung up. For example, a short-term loan for an expensive dinner to be repaid in one week or a loan required by a DJ (Disco Jockey) to buy equipment. Currently, this is mostly managed by credit card usage and payments in instalments.

However, there is ample scope for innovative, low cost, low corpus, high volume, and high creditworthy loan disbursements. Such smaller amounts expand the horizons available to FinTech start-ups specialising in lending. Established institutes such as SIDBI have been joined by a flourish of FinTech initiatives both from start-ups such as Lending Kart, and erstwhile traditional firms like Capital First.

At the other end, relatively easy availability of institutional capital has made way for start-ups to create short-term loan offerings to individuals. The PMMDY guidelines issued by Department of Financial Services indicate that all banks are required to lend to micro enterprises engaged in manufacturing, processing, trading and service sector activities.

Innovative short-term financing solutions will need innovative credit scoring mechanisms. Current advances in technology and access is elevating more and more individuals from the informal into the formal sector – for example, Ola/Uber driver information or Amazon/Flipkart vendor information. Ample and diversified data from this migration as also through GST, IndiaStack applications, etc. allows lenders to slice and dice the data, thus creating their own unique credit models. This analysis can be used to create innovative, yet functional credit scoring systems.

Banking Tech: Regulatory push; Need for technology support by traditional banks

If there is one thing the government is very vocal about, it is including as much of the population as is possible into the financial system. The Aadhaar drive along with Jan Dhan Yojana is only a first step towards this aim. This is to both, collect complete data and make sure government subsidies reach beneficiaries with as little friction as is possible.

The resultant increase in population with bank accounts has created a need for an upgrade in banking technology infrastructure. The additional schemes of Pradhan Mantri Suraksha Bima Yojna (group life insurance term plan), Pradhan Mantri Jeevan Jyoti Bima Yojana (accident insurance plan) and Atal Pension Yojna (benefit pension product) have generated scope for financial services even in the population from the lowest income strata.

Further, recent changes in licensinhave opened some aspects of banking to non-financial institutions. Payment bank licenses accorded to non-traditional financial services such as a wallet firm, Paytm or a Telecom company, Airtel validate this push.

Towards the aim of making financial transactions seamless, there is a regulatory push towards common transaction backbones, such as UPI. This has forced banks to adapt to newer technology. While they could choose to build the required technology in-house, there is potential for start-ups to become solution providers to banks.

Consumer Finance: Complex regulation; Needs further penetration

Increase in household spending from $873 million in 2010 to $1.3 trillion[7] in 2015, driven in part by a steady increase in Median Household Incomes has made consumer finance products even more indispensable. Historically, banks favoured loans to individuals – mortgage, vehicle or personal – over institutional and SME loans.

This enabled innovation in the consumer finance arena by players such as Bajaj Capital, Yes Bank, SBI. They captured consumers with spending on durables at payment point itself through EMI, pre-approved loans, etc.

In addition, even a regular mandatory process such as Tax filing was very cumbersome before the inception of start-ups like ClearTax who are finding increasing uptake for their services.

BlockChain: Successful experiment; Needs the attention it deserves

BlockChain, the distributed, self-regulating, transparent, immutable database concept that has taken the financial world by storm is an infant waiting to be nurtured and moulded.

Large banks have been experimenting to adopt the Distributed Ledger technology. SBI has started “BankChain” in partnership with IBM, Microsoft, Skylark, KPMG and 10 other commercial banks to share information to prevent fraud and bad loans. Banks such as Axis bank are also looking to leverage Blockchain to improve interbank trade finance processes.

Even a non-traditional, funding company Mahindra has tied up with IBM[8] to use Blockchain to improve its supply chain finance business, as has Bajaj Electricals/Yes Bank. The Institute for Development and Research in Banking Technology had a successful “proof of concept” that involved multiple banks such as SBI to test the Blockchain implementation of trade finance settlements.

We expect incumbents and start-ups to continue exploring new opportunities and paradigms in re-imagining current business processes using Blockchain and the regulator to continue providing encouragement with light touch regulation on all aspects of Blockchain usage (except crypto-currency).

Insurance Tech: New technology, big data; Need for new insurance models

Increase in use of wearables, detailed patient record-keeping with improved diagnostics have forced insurance to go digital too. Richer data on public health in combination with better analytical tools leaves the ground open for personalised insurance services.

Similar to the banking sector, the big insurance players are also adapting by creating in-house competency or assimilating start-ups that can help them take the leap. SwissRe had an intensive accelerator programme for start-ups in the space. In addition, auxiliary health services such as corporate fitness plans and alternate medicine/therapies have made it easier to add and measure premiums.

The Insurance Tech space in India is mostly covered with aggregators and marketplace for insurance providers rather than innovative (re)insurance offerings. The increased penetration of mobile internet, maturity of non-institutional transactions, and reliable consumer credit profiles can help develop new insurance models that service both individuals and small retailers – for example, OneAssist provides insurance against mobile phone loss/theft, Friendsurance in Germany offers P2P insurance, consumer durables insurance, etc.

Enterprise Finance: Growing number of SME; Needs players to address SME requirements

A favourable market has boosted the number of businesses started each year with the total number reaching 51 million out of which only 32% are digitally engaged. The public sector banks are unable to keep pace with credit demand growth arising from rising GDP. This has led to a wave of start-ups supported by deep pocket investors.

They provide for SME sector’s short-term financing needs through multiple products such as invoice financing, bill discounting, loan against property, cash-flow based financing. Growth in e-commerce too has paved the way for aggregating retail sellers and small businesses and streamlining their financial operations as is done by companies such as CapitalFloat, LendingKart.

Investment Tech: Growing target audience; Needs new-age implementation

With the tech-savvy population – the millennials – getting into the “earning” phase of their lives, there is an increase in awareness of various investment options. This has created a need for investment marketplaces and advisers. Relatively smaller cases but successful stories nevertheless, ScripBox and Zerodha cater to retail investors with high-tech analytics and simple, convenient user interface.

In addition, data analytics lends itself to AI-assisted platforms that create more trust in investment services. They also make personalised investment advice, automated and intelligent portfolio monitoring and management possible.

Each FinTech sub-vertical has had supporting enablers that helped start-ups take advantage. Unsurprisingly, each sub-domain has driving factors that can help exploit the further potential. The categorization of the FinTech space thus segregates sub-sectors that are ahead on the curve from the ones that need to catch-up with the world, with potential to even surpass the global status.

Also Read: Mobile Wallet Industry in India: Are We Asking the Right Questions?

(Disclaimer: This is a guest post submitted on Techstory by the mentioned authors. All the contents and images in the article have been provided to Techstory by the authors of the article. Techstory is not responsible or liable for any content in this article.)

About The Authors:

{kind=link}