Over the past two decades, India has pushed hard to become a less–cash society. India has made significant financial inclusion advancement in the past two years, but cash is still presiding. The payments sector in India is evolving fast, offering customers with myriad choices to make payments by integrating it well with mobility (smartphones, apps), cloud tech and by expanding its reach to sectors like retail, entertainment and others. It’s like a rolling stone gaining momentum every month. Some people say that it’s the next big sector after E Commerce for India and its entrepreneurs.

FinTech is disrupting consumer finance by providing people better access to spending, credit and investing information for them to make rational decisions. India is seeing a new breed of tech-savvy and hungry entrepreneurs who are looking to solve big problems. They are increasingly focusing on customer experience which acts as a differentiator compared to banks. FinTech startups’ efforts are focused on simplifying and innovating transactions in the digital platform so that they can rapidly change the way customers are transacting.

A quick look at the Indian consumer financial landscape, especially Digital payments, which gives a fresh hope of optimism.

Some data to focus on:

- According to a recent report by GrowthPraxis, the market for mobile enabled payments in India has grown more than 15 times to reach its current size of US$ 1.4 billion by the end of FY’15 from US$ 90 million at the end of FY’12.

- If we compare urban and rural households, about 11% of the urban households are involved in making cashless payments whereas 0.43% of rural households make cashless payments.

- Mobile payments have grown from USD 88 million in 2011 to USD 1.15 billion in 2016, a compound annual growth rate of 68 percent

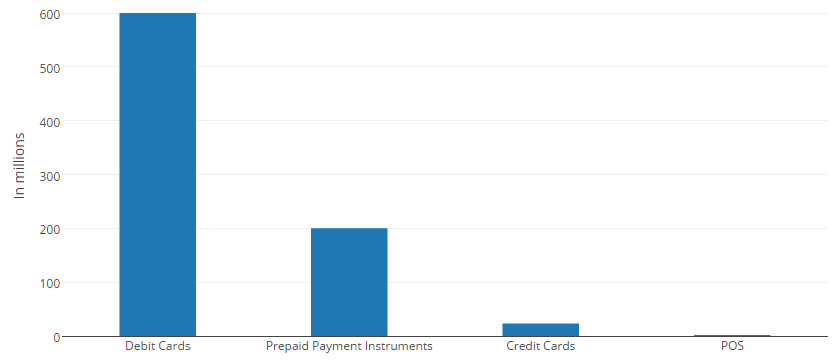

- As of March 2016:

Government Initiatives

Keen interest from the government to reduce cash transactions is seen as a major positive factor for FinTech entrepreneurs.

- The Government of India has encouraged the shift to a less–cash society with its push for digital payments through the JAM Trinity: the Prime Minister’s Jan-Dhan Yojana, Aadhaar, and mobile connectivity. With PMJDY, 22.31 crore accounts opened with 38k crore in float balance

- The vision of Digital India, a flagship programme of the Government of India, is to promote mobile and digital banking to encourage financial inclusion.

- New Government initiatives such as the Unified Payments Interface and Aadhaar – are examples of the big changes under way.

- Inclusion of Imminent ‘India Stack’ will surely boost the customer onboarding on these payment channels.

- Today, efforts to improve financial literacy are undertaken by the central bank as well as by banks, microfinance institutions, and institutions like the National Bank for Agriculture and Rural Development (NABARD), the National Stock Exchange, the Bombay Stock Exchange, and the Securities and Exchange Board of India.

- Some of its marquee efforts by Indian Government to bolster the payments industry are Introduction of platforms like the Bharat Bill Payment Systems and the National Payments Corporation of India’s Unified Payments Interface.

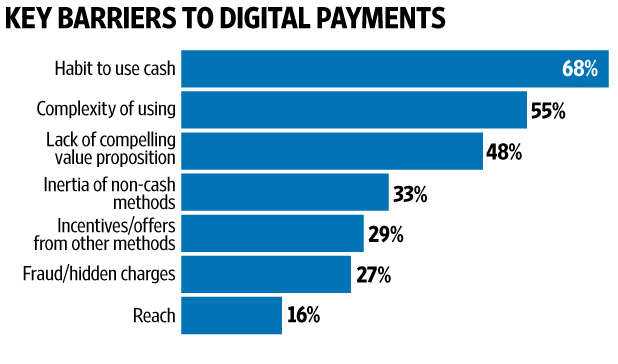

Why India love transacting in cash so much ?

Merchant adoption in Digital payments

There is an Insufficient focus on financial literacy. Merchants don’t fully understand and appreciate the benefits of the efficiencies and security of electronic payments relative to cash payments. Apparent lack of readiness of merchants to interoperate in order to adopt the technology at a large-scale. Also they lack interest in leveraging the benefits of cashless transactions v/s cash based transactions.

Also, Merchants and cardholders fear the security risks of paying electronically. increasing the use of digital payments between merchants and consumers is a chicken-and-egg dilemma. Merchants and consumers blame each other for not demanding and accepting digital payments respectively.

How to accelerate growth of Digital payment in India and increase adoption of digital payments?

- Expand acceptance and Government Initiatives: India is in transition in both the areas of acceptance penetration and consumer adoption. Over the last few years, India has undertaken measures to begin the shift to a less-cash society. However, single-digit debit card activation rates and a large shadow economy deserve the need for continued intervention by Indian Government. The establishment of Small Finance and Payments Banks, the launch of the government’s Start-Up India, will surely accelerate the acceptance and adoption.

- Demonstrating the effectiveness of digital payments for high-frequency low-value transactions will compel more and more mobile users to install m-wallets. For mobile payments, we need to seek a suitable three-way compromise between security, convenience and cost.

- A rapidly growing fintech sector – has the potential to dismantle barriers to digital payments. All these developments provide India with a unique opportunity to leapfrog and move quickly to a digitally enabled payment system.

Taking advantage of advances of these kinds would help India meet its objectives of promoting financial inclusion. Mobile payment service providers and banks need to work together to create a seamless ecosystem for the technology to work efficiently.

All in all, Digital payments will play a critical role in achieving the Digital India vision and in driving financial inclusion. With low but rapidly increasing levels of digital/Internet penetration incorporated with the government initiatives, is attracting investments and interest in FinTech.

Young entrepreneurs have taken this challenge and have created and expanded some promising start-ups in India. The progress like this could be game changer for India. The problem is that this drumbeat has been going on for last few years, yet little seems to change. The promise of financial inclusion in India has been for long time but has never materialised. The key questions are “why?” and “might we need a fresh approach?”

(Disclaimer: This is a guest post submitted on Techstory by the mentioned authors. All the contents and images in the article have been provided to Techstory by the authors of the article. Techstory is not responsible or liable for any content in this article.)

About the Author:

This article is contributed by Fatima Bohra, working at a global Venture Capital firm Idein Ventures which has invested in multiple hybrid E-commerce companies.

This article is contributed by Fatima Bohra, working at a global Venture Capital firm Idein Ventures which has invested in multiple hybrid E-commerce companies.

She is an analyst by day and a reader by night. Tech & Startup enthusiast by mind and an amateur chef by heart.

{kind=link}