What Is an Amended Return?

An amended return is a structure recorded to make remedies to an expense form from an earlier year. An amended return can address blunders and guarantee a more profitable duty status, like a discount. For instance, one could decide to document an amended return in cases of distorted profit or tax reductions. Numerical mistakes, be that as it may, don’t need alterations because the IRS consequently rectifies such blunders while handling the assessment form.

Who Ought to Record an Amended Return?

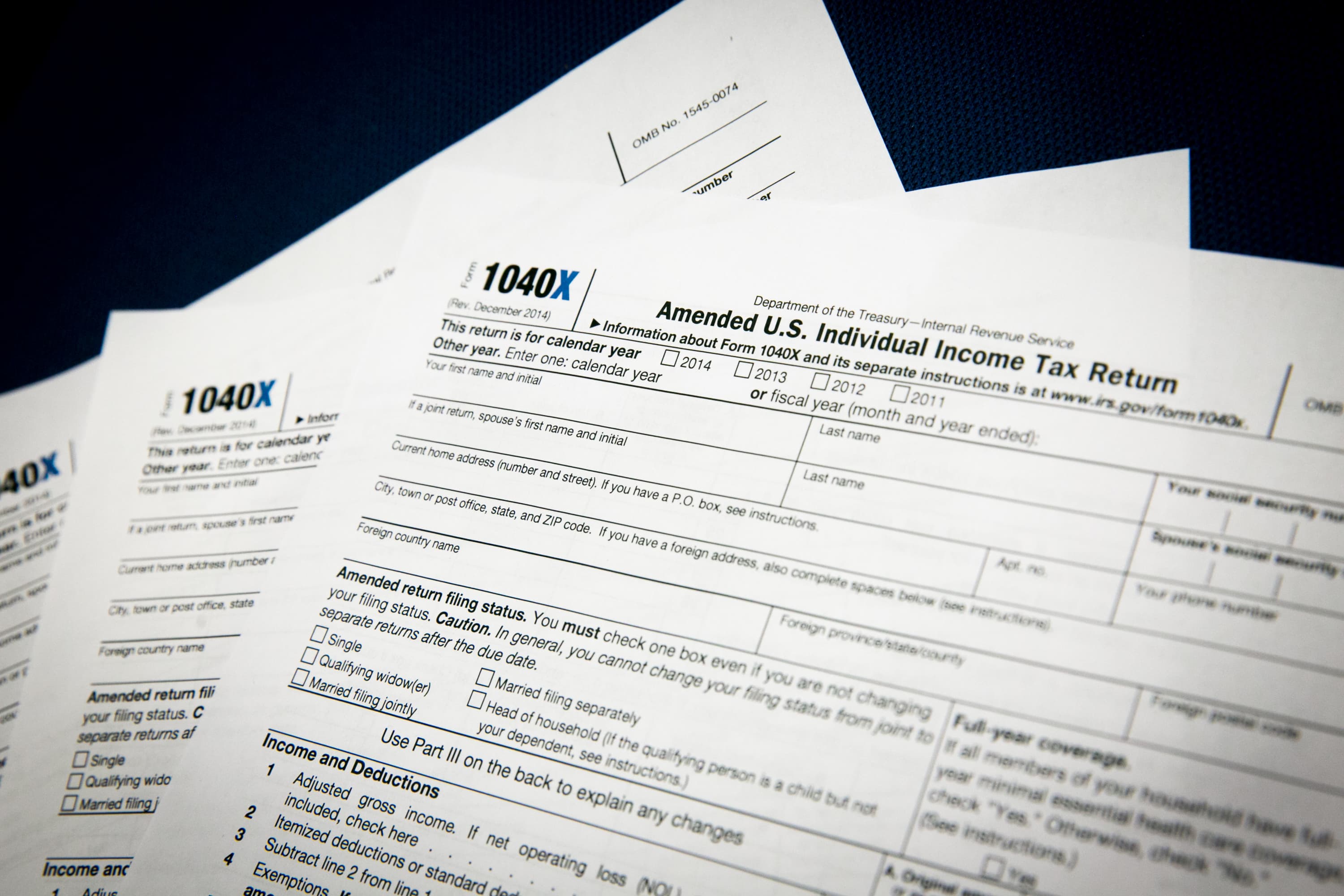

All citizens are expected to document their expenses yearly for the past fiscal year. Citizens might understand that they committed an error in finishing up their tax documents, or their conditions might have changed after they have submitted or sent a return that has been acknowledged by the public authority. On the off chance that this happens, the Inside Income Administration (IRS) has given a way for these people to re-try their expenses by giving an amended return structure, Structure 1040-X, on the IRS site.

An amended assessment form can be recorded even after the duty documenting cutoff time for the fiscal year has passed.

Not all blunders need altering by the structure. The IRS will detect and address a numerical mistake, for instance, when the underlying expense form is sent in for handling. At the point when this occurs, any discount owed will be changed and any additional duty risk due will be charged to the citizen. If the individual neglects to remember an expected structure or timetable for their submitted unique assessment form, the IRS will send a letter mentioning that they mail the missing data to one of their workplaces.

When to Record an Amended Return

A citizen should record an amended return if:

The citizen’s recording status for the fiscal year changed or was mistakenly placed. For instance, on the off chance that an individual recorded as single but got hitched on the last day of the fiscal year, they should correct their return by documenting their duties under the fitting status — wedded recording mutually (MFJ) or wedded recording independently (MFS).

The quantity of wards guaranteed is mistaken. An amended return will be vital assuming a citizen needs to guarantee extra wards or eliminate wards that were recently asserted. For instance, a couple might have incorporated a child brought into the world in January before charges were recorded in April on the earlier year’s assessment form. That child can’t be remembered for the earlier year’s expense form since they were not brought into the world before the year’s end.

Tax breaks and derivations were guaranteed mistakenly or were not asserted. In the last option case, the citizen might have understood that they qualified for credit or derivation and might need to record an amended re-visitation to mirror this.

The pay detailed for the fiscal year was inaccurate. If a citizen gets extra expense records for the fiscal year (say a Structure 1099 or a K-1 shows up via the post office after the duty cutoff time), they might document an amended expense form to report the extra pay.

Deductibility of specific costs changes because of regulation changes. Some of time, regulation will come through after a citizen has recorded a return that influences the deductibility of specific costs. For instance, the derivation for private home loan protection (PMI) was initially terminated on Dec. 31, 2017, because of the Tax reductions and Occupations Demonstration of 2017. The Combined Assignments Act, endorsed into regulation in December 2019, expanded the derivation through Dec. 31, 2020. This made the derivation accessible for the 2019 and 2020 fiscal years and retroactive for the 2018 fiscal year.

Charge help because a catastrophic event changes the citizen’s duty risk. This is a typical issue for citizens who have been impacted by a cataclysmic event, particularly one in the later piece of the fiscal year. The public authority much of the time offers charge help for those impacted by catastrophic events, however, regulation might take more time to conclude than the common expense season window permits. Citizens ought to pay their full expense obligation as it sits when the government form is expected. If regulation changes, an amended return can be documented to recover any discount owed to them because of cataclysmic event charge alleviation.

The citizen understands that they owe a larger number of duties than they paid. To try not to get hit with a punishment from the public authority, they can record an amended return with the IRS.

Instructions to Revise a Government form

Structure 1040-X has three segments: A, B, and C. Under segment A, the figure that was accounted for in the first or last-amended tax document is recorded. The citizen should enter the changed or right number in section C. The distinction between sections An and C is reflected in segment B. The changes made to a government form will either bring about a duty discount, funds to be paid, or no expense change. The citizen likewise needs to make sense of what transforms they are making and the purposes behind rolling out every improvement in a segment given on the rear of Structure 1040-X.

{kind=link}