Entrepreneurs today have many options when it comes to raising money to fund their startup. If you are looking at debt investment as a possible source of capital, here are some things that will definitely help you out. But before we jump in right into the game, let us look at a few fundamentals about this less frequent jargon ‘Debt Investment’ in the Indian market.

What is Debt Investment?

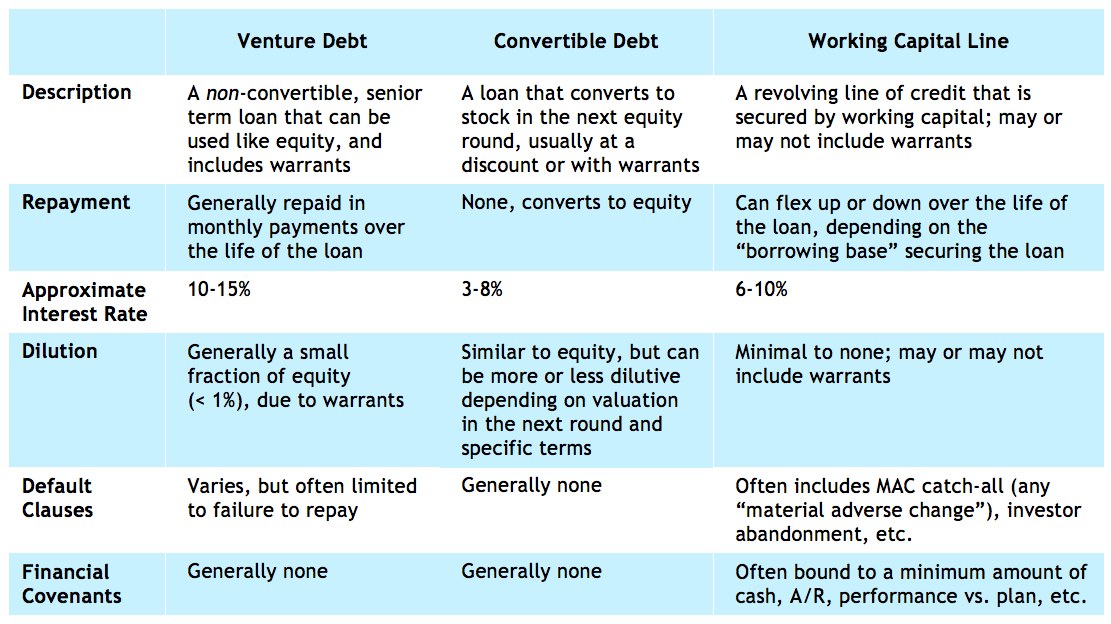

Debt investment is a loan which must be paid back within an agreed period of time, with interest. It is most commonly used during Seed Investment Rounds and during Bridge rounds, led by a Venture Capital firm, in order to get a company from a Series A to a Series B to a Series C level funding.

Debt investment is used in order to lessen dilution of the company’s founders and existing investors, because every time equity is issued, existing investors share becomes smaller and smaller.

A lot of startups prefer to use a combination of debt financing and equity financing as they grow. If you are opting for debt investment model, both debt and equity together is the prudent approach followed by startups.

The Different Sources of Debt Investment

Just like how equity investments is not from a single sources, but can be raised from multiple sources such as friends and family, angel investors, venture capital, hedge funds etc., even debt investments can be raised from multiple sources as well.

1. Loan from Banks & NBFCs

Loans from banks and Non-Banking Financial Companies (NBFCs) can be used as debt investments by startups to purchase inventory and equipment in addition to being used as operating capital and funds for expansion. But, on the flip side, they require substantial collateral and a good track record, besides the fulfillment of other terms and conditions and a lot of documentation. The debt investment will have to be paid back within a stipulated time, regardless of how your startup is faring

2. External Commercial Borrowings

External Commercial Borrowings (ECB) in form of buyers’ credit, bank loans, suppliers’ credit, securitized instruments such as floating rate notes, fixed rate bonds or non-convertible or optionally convertible or partially convertible preference shares, can also be availed as debt investment. ECBs have certain end use restrictions such as that it cannot be used for on-lending or investment in capital market, acquiring a company, real estate sector etc.

3. CGTMSE Loans

Entrepreneurs can get debt investment as loans of up to 1 Crore, under the Credit Guarantee Trust for Micro and Small Enterprises (CGTMSE) scheme. This is an initiative launched by Ministry of Micro, Small & Medium Enterprises (MSME), Government of India. The loans are issued without collateral or surety. Any new and existing micro and small enterprise can avail the loan under this scheme from all scheduled commercial banks, certain Regional Rural Banks, National Small Industries Corporation Limited (NSIC) and Small Industries Development Bank of India (SIDBI), which have signed an agreement with the Credit Guarantee Trust.

Then there is the concept of convertible debt. Convertible debt is issued like debt, as a loan with an interest rate and a repayment period. However, at the end of the specified repayment period or at an agreed upon milestone this debt converts into equity ownership.

Also Read: How To Negotiate Better During Your Startup Funding Process

When to use debt investment to fund your startup

Debt investment makes sense when a startup does not experience expected success. In a debt investment model, investors get returns for their investment, as periodic payments. If all goes well, the startup will repay the debt in full, plus interest payments, as per an agreed-upon time frame.

In worst-case scenarios, a debt investment model prevents investors from losing the entire amount they’ve put into a company. This is bad news from the point of view of the entrepreneurs, since venture debt must be repaid before all other debt if the startup is forced into liquidation or bankruptcy.

Drawbacks of debt as a funding source

- In order to ensure regular repayment to investors, a company may have to forego a needed expansion or liquidate assets crucial to future growth.

- Debt investment may leave your startup vulnerable during hard times.

- In some cases, the company may be forced into bankruptcy and be required to liquidate all assets.

When to use convertible debt to fund your startup

Convertible debt, allows for a quick turnaround so business owners can get back to running their business. Also, unlike regular debt investment, convertible debt does not involve monthly repayment. Instead, the principal amount of the loan plus all accumulated interest converts to equity at the end of the loan period. This means that entrepreneurs don’t have to worry about the monthly cash flow restrictions of debt investment. The major advantage of issuing convertible debt is that it is inexpensive and easy to execute.

Drawback of convertible debt as a funding source

Although there aren’t many, one key drawback of convertible debt as a funding resource is that the investor doesn’t know exactly what the deal will ultimately look like until the agreed upon milestone.

When to use equity investment to fund your startup

Equity is most commonly issued in order to lessen cash flow risk associated with the interest payments on debt.

Equity investment allows for a lot of flexibility. This can prove to be advantageous since it allows the startup to place more resources back into the business, whereas debt investment restricts cash flow by mandating that investors get paid back on a regular schedule. It also enables the startup to grow at a faster rate.

Equity investment allows for a lot of flexibility. This can prove to be advantageous since it allows the startup to place more resources back into the business, whereas debt investment restricts cash flow by mandating that investors get paid back on a regular schedule. It also enables the startup to grow at a faster rate.

As long as those investing in equity are willing to wait, the return on their investment grows alongside the company they back.

Drawbacks of equity as a funding source

- Each time an additional round of investment introduces new shares; earlier shares are diluted and.

- Equity deals usually take longer to close and have higher legal costs than those of debt financing.

No investment structure is perfect. If a startup remains without external funding for too long, it may be unable to take advantage of market opportunities.

While the plethora of lending options may make it easier than ever to get started, responsible entrepreneurs should focus on the big picture and the long term objectives.

Also Read: Do You Know How SAFE Can Be Your Startup Funding?

{kind=link}