Do you also worry about how a potential recession or even an economic slowdown might affect you as well as your finances? Now, assuming that you have some time to prepare, which indeed is not always the case, you can actually put your fears to rest as there are a lot of everyday habits the average person can implement in order to protect themselves ahead of time from the sting of recession or make it such that, you won’t really feel its effects at all. All in all, there are tools and methods which can actually help you get through it in one piece, financially speaking of course!

Before moving any further, I sincerely believe that it is best if we first have a brief look at what recession really is as some of you might not be very well versed with the concept and this would really help you have a much better understanding of the topic and what we have with us next.

What is a Recession?

So, to begin with, a recession is nothing but simply a macroeconomic term that usually refers to a significant decline in the general economic activity in a designated region of course. In other words, a recession is a period of declining economic performance across an entire economy that is known to last more than a few months, usually visible in normal GDP, employment, wholesale-retail sales, real income as well as industrial production of course.

On a similar note, investors, businesses as well as government officials track various economic indicators that can help a lot in predicting or even confirming the onset of recessions but, it is worth noting that, they are officially declared by the National Bureau of Economic Research (NBER).

Now, as mentioned, such a slowdown in economic activities may last for some quarters thereby completely hampering the overall growth of the economy. In such a situation, all of these economic indicators fall. As a result, this creates a rather big mess in the entire economy, and in order to tackle the menace, economies generally react by simply loosening their monetary policies by infusing more money into the system, i.e by increasing the money supply.

Lastly, this is done by reducing the interest rates. Increased spending by government and decreased taxation are also considered good answers to this problem. The recession which hit the globe in 2008 is the most recent example of a recession.

Though there are a variety of economic theories that have been developed in order to explain how and why exactly recession occurs, but I think you get the gist of the whole thing!

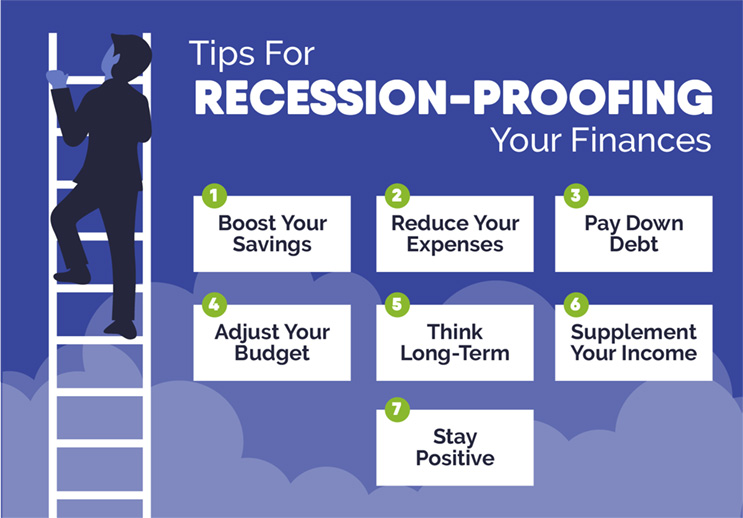

Top financial tips to save you from recession

1. Diversify your investments:

Simply speaking, if you don’t have all your money in one place, your chances of losing all your money at once also reduces significantly. An easy example of this is, say you own a house and you have a savings account, so congratulations, you are now having money in the bank as well as in a real estate.

Basically, all I want to convey is to build a portfolio of investment pairs that are not very strongly correlated, meaning that when one is up, the other is down and vice versa and so, in a time of necessity or recession for instance, you will be on a safe side financially.

2. Live within your means:

We usually see that people don’t always live within their means and always want more than what they can afford perhaps. If you make it a habit of sorts to live within your means every day of your life, even during the good times, you are even less likely to go into debt when gas or food prices go up and more likely to be adjusting your spending in other areas to compensate.

It’s simple, debt begets debt when you don’t have the capacity to pay it off right away. Especially in a time of recession, I don’t think paying off debt should be your concern because you will first have to think about fulfilling your necessities and so, not having debt or something that you have the resources to pay off easily is the way to go about it. Reduces the overall expense and leaves you with more cash in hand. So, living with what you have and within your means is what will help keep the peace of mind in such times.

3. Have additional income:

Even if you are lucky to have a full-time job, which pays you good money for you to manage your expenses, it is never a bad idea to have a source of extra income on the side. This income could be of anything, from a consulting work or selling collectibles on eBay. Since job security is non-existent these days, you should start diversifying your streams of income as well as your investments for sure.

If say recession hits, if you lose money in one stream, you still will have the other one. Yeah, of course, you won’t be getting what you were from your primary job but at least you have a recurring income.

4. Have an emergency fund:

Imagine you have plenty of cash lying around in a rather high-interest a bank or a federal deposit insurance corporation (FDIC) insured account, not only will that money of yours retain its full value in a time of such turmoil, but moreover over it will also be extremely liquid, thus giving you easy access to funds if in case you lose your job or are forced to take a pay cut for that matter, like in the times of recent global Covid-19 pandemic.

Furthermore, having money also means that, you will have less dependency on borrowed funds and it is worth noting that, credit availability usually tends to dry up quickly as recession hits and so, having such reserved funds would help fulfill your necessities.

5. Invest for the long term:

It is always good to have certain long-term investments. It doesn’t really matter if your current investment comes down to 15 percent or less but all we know is that the market is critical and in the long run, the prices will increase and you will have plenty of opportunities to sell high. Also, to have a profitable investment, I would say, buy when the market is at its lowest.

Having said that, after retirement or in the case of a recession, you will still have your investments to liquidate in order to take care of your expenses and know that, the more you let it be and the longer the investment is made for, the more the return would be. It’s just that you will have to see the right time to cash out your investments.

6. Be aware of your risk tolerance:

There are a lot of experts and gurus in the field of finance who say that a person of a certain age should have portfolios allocated In a certain way. However, if you are unable to have a peaceful sleep at night then what is the use of all this. Your investments are a way for you to feel financially secure and not stressed.

Say you have extra cash lying around and you decide to adjust your allocation when the market is down, you can even be able to earn certain profits but in the long run of course or otherwise, you would have to be very good at what to sell and when to sell if you are in need to make money in a shorter while.

Though you have to still be a little careful about your risk tolerance as that would cause you to make rather poor investment decisions. Even if you are in the age bracket of having a portfolio with 80 percent in stocks and about 20 percent in bonds, you would never be able to actually see the returns that advisors intend if you sell when the market is down. It is a game for the long term.

7. Keep your credit score high:

When credit markets together, in order to get approved to take a credit card or a type of loan, you will have to have a rather excellent credit score. Now, if you are wondering as to how exactly can you raise or maintain your credit score? It all really depends on things like paying your bills on time as well as keeping your oldest credit cards open along with a lot more if you want to have a high credit score. As a result, when times get tough, this credit score of yours will help you have some amount of financial security.

8. Create two budgets:

Yes, it is rather necessary to build out two budgets, one for today, a normal working day when you are earning your standard income and everything is going smoothly and one for doomsday as that would really help you have everything planned in your head for as to what all expenses you can easily shed to have money left to fulfill your necessities. Like your groceries, transportation, as well as rent are things you need to pay for but Netflix for instance gym memberships are something that you can cut off to save money and have resources left to survive.

9. Assess your financial situation before paying off debt:

Yes, as difficult as it may be, you need o actually access your financial situation before you go ahead paying off all your debt because it should not be the case that when you are done, you are left with nothing and you again have to take loans. Also, it should neither be the case that you are not paying off a high-interest credit balance and so, it could be your extra expense. All in all, it is very important to find the right balance between the two in order to sustain when times get hard.

10. Invest in your value as an employee:

We all know that recessions do cost jobs and in great recessions, numerous sectors are negatively impacted. As a result, it is important to make sure that your resume is up to date and that you go above and beyond in order to show your value to your employer and prospective hiring managers as well. Show that, you can manage your work well and can also diversify yourself and work or coordinate with other departments. This is how you can actually secure your job when a recession hits and be on the safe side.

Reading so far, I hope you have gotten a fair insight into some of the most popular financial tips to save you in the case of recession and now I believe you would be able to decide on your own whether or not you should follow such tips and tricks to maintain your financial stability.

In conclusion, what are your thoughts on the Top 10 financial tips to save you from a recession? Do let us know in the comments area below. To know more about such reports, do check out other articles we have on our website. Thank you for your time & if you found our content informative, do share it with your investor friends!

Also read: How does Ola make money? Ola’s business model is explained!

{kind=link}